Occupational pensions, macroprudential limits and the financial position of the self-employed

“Tighter borrowing restrictions in the mortgage market do not crowd out additional pension saving for self-employed”

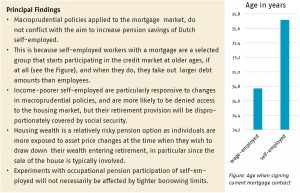

Tightened borrowing restrictions, such as lower macroprudential limits on the loan-tovalue ratio or the debt-service-to-income ratio, make it relatively harder for many Dutch households to obtain a mortgage in recent years. We find no contradiction to the current policy aim of increasing pension saving of self-employed individuals. Whereas the self-employed are less likely to get a mortgage, and their borrowing is more sensitive to changes in restrictions compared to employees, in particular at the lower end of the income distribution, those self-employed that succeed to borrow tend to be older and wealthier, and they borrow more. However, the larger debt positions of the self-employed, before retirement, are associated with higher undiversifiable risk of a housing market downturn.

Key Takeaways for the Industry

- Low-income, self-employed individuals would enjoy limited benefits from an occupational pension as social security (AOW) offers decent replacement rates for lower incomes.

- Middle- and high-income self-employed individuals could benefit from an occupational pension without incurring extra debt even if borrowing limits are prudentially set.