Variable annuities with financial risk and longevity risk in the decumulation phase of Dutch DC products

“Exploring the risks and benefits of variable pension products to facilitate pension choices”

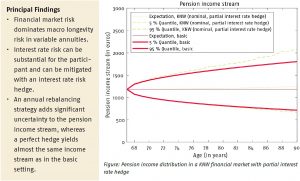

Guaranteed pension products are increasingly unsustainable and so alternatives are being sought. Dutch defined contribution schemes allow investment risks to be taken during retirement. Such variable annuity products can yield a higher first pension payment compared to a fixed annuity product without equity exposure, but carry the risk of an uncertain pension income. Recent Dutch legislation requires pension providers to explain these risks, but this law does not cover every risk. This study develops a general framework that quantifies all such risks (stock market, interest rate, inflation and longevity).

Key Takeaways for the Industry

- Incorporating financial shock smoothing for a long enough period in pension products can reduce the average year on year volatility of pension income by a factor of three compared to a basic variable annuity.

- Longevity risk should be included in consumer information so that participants can make a well-informed choice between a fixed and variable annuity.

Need to know more?

Read the paper “Variable annuities with financial risk and longevity risk in the decumulation phase of Dutch DC products” by Bart Dees, Frank de Jong and Theo Nijman (Tilburg University).